Updated Investor Bulletin: How Fees and Expenses Affect Your Investment Portfolio

June 26, 2019

The SEC’s Office of Investor Education and Advocacy is issuing this updated bulletin to educate investors about how fees you pay for investment services and products can impact the value of your portfolio.

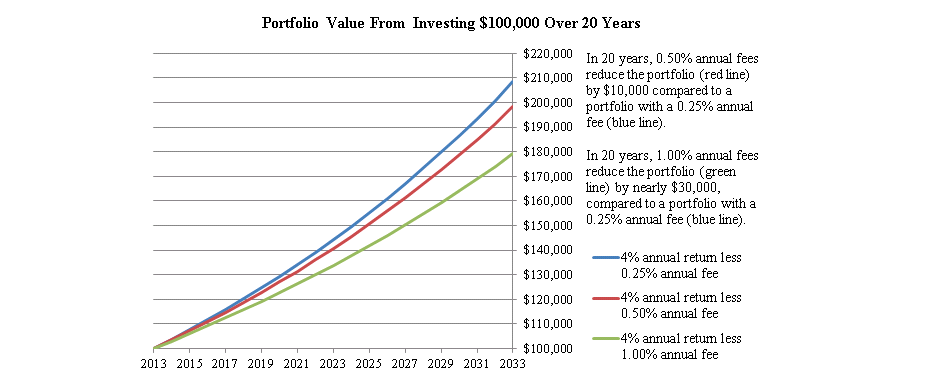

As with anything you buy, there are fees and costs associated with investment products and services. These fees may seem small, but over time they can have a major impact on your investment portfolio. The following chart shows an investment portfolio with a 4% annual return over 20 years when the investment either has an ongoing fee of 0.25%, 0.50% or 1%. Notice how the fees affect the investment portfolio over 20 years.

Along with the other factors you think about when choosing either an investment professional or a particular investment, be sure you understand and compare the fees you’ll be charged. It could save you a lot of money in the long run.

How do I know what I’m being charged?

- Get informed. Find out what you may be charged by reading what your investment professional provides you. For example, look at your account opening documents, account statements, confirmations and any product-specific documents to see the types and amount of fees you are paying. Fees impact your investment, so it’s important you understand them.

- Ask questions so that you understand what you will be charged, when and why. Questions might include:

- What are all the fees relating to this account that I will be charged directly or indirectly? Do you have a fee schedule that lists all of the fees that will be charged for investments and maintenance of this account?

- What fees will I pay to purchase, hold and sell this investment? Will those fees appear clearly on my account statement or my confirmation? If not, how will I know about them?

- How can I reduce or eliminate some of the fees I’ll pay? For example, can I buy the investment directly without paying an investment professional? Can I pay lower fees if I open a different type of account?

- Do I need to keep a minimum account balance to avoid certain fees?

- Are there any other transaction or advisory fees? Account transfer, account inactivity, wire transfer fees or any other fees?

- How do the fees and expenses of the product compare to other products that can help me meet my objectives?

- Does the product have more than one share class? If so, how do the fees compare across share classes? What is the overall lowest cost share class available and how do I qualify for that share class?

- How much does the investment have to increase in value before I break even?

- Ask questions about your investment professional’s compensation. Questions might include:

- How do you get paid? By commission? How are commissions determined? Do they vary depending on the amount of assets you manage?

- Do you get paid through means other than through commissions and amount of assets you manage and, if yes, how?

- Do I have any choice on how to pay you?

- Check your statements. Review confirmation and account statements to be sure you’re being charged correctly and ask your investment professional to break the fees down for you if it’s unclear.

What types of fees are there?

Fees typically come in two types—transaction fees and ongoing fees. Transaction fees are charged each time you enter into a transaction, for example, when you buy a stock or mutual fund. In contrast, ongoing fees or expenses are charges you incur regularly, such as an annual account maintenance fee.

How do transaction fees affect your investment portfolio?

Transaction fees are charged at the time you buy, sell or exchange an investment. As with any fee, transaction fees will reduce the overall amount of your investment portfolio.

How do ongoing fees affect your investment portfolio?

Ongoing fees also reduce the value of your investment portfolio. This is particularly true over time, because not only is your investment balance reduced by the fee, but you also lose any return you would have earned on that fee. Over time, even ongoing fees that are small can have a big impact on your investment portfolio. The chart above illustrates the effect of different ongoing fees on a $100,000 investment portfolio with a 4% annual return over 20 years.

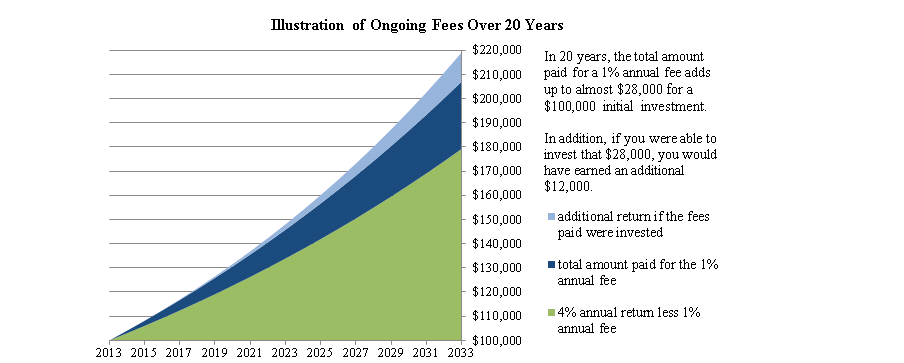

The chart below illustrates the impact of a 1% ongoing fee on a $100,000 investment portfolio that grows 4% annually over 20 years. As the investment portfolio grows over time, so does the total amount of fees you pay. Because of the fees you pay, you have a smaller amount invested that is earning a return.

What is an example of a transaction fee?

Commissions. You will likely pay a commission when you buy or sell a stock through an investment professional. The commission compensates the investment professional and his or her firm when it is acting as agent for you in your securities transaction.

Markups. When a broker-dealer sells to you directly securities it holds, the broker-dealer acts as a principal in the transaction. When acting as a principal the broker-dealer generally will be compensated by selling the security to you at a price that is higher than the market price (the difference is called a markup), or by buying the security from you at a price that is lower than the market price (the difference is called a markdown).

Sales loads. Some mutual funds charge a fee called a sales load. Sales loads serve a similar purpose to commissions by compensating the investment professional for selling the mutual fund to you. Sales loads can be front-end in that they are assessed at the time you make your investment or back-end in that you are assessed the charge if you sell the mutual fund usually within a specified timeframe.

Surrender charges. Early withdrawal from a variable annuity investment (typically within six to eight years, but sometimes as long as 10 years) will usually result in a surrender charge. This charge compensates your investment professional for selling the variable annuity to you. Generally, the surrender charge is a percentage of the amount withdrawn, and declines gradually over a period of several years.

What is an example of an ongoing fee?

Investment advisory fees. If you use an investment adviser to manage your investment portfolio, your adviser may charge you an ongoing annual fee based on the value of your portfolio.

Annual operating expenses. Mutual funds and exchange-traded funds, or ETFs, are essentially investment products created and managed by investment professionals. The management and marketing of these investment products result in expenses and costs that are often passed on to you—the investor—in the form of fees deducted from the fund’s assets. These annual ongoing fees can include management fees, 12b-1 or distribution (and/or service) fees, and other expenses. These fees are often identified as a percentage of the fund’s assets—the fund’s expense ratio (identified in the fund’s prospectus as the total annual fund operating expenses).

401(k) fees. The expenses for operating and administering 401(k) plans may be passed along to its participants. This is in addition to the annual operating expenses of the mutual fund investments that you may hold in your plan.

Annual variable annuity fees. If you invest in a variable annuity, you may be charged fees to cover the expenses of administering the variable annuity. You also may pay fees such as insurance fees and fees for optional features (often called riders). You will also be subject to the annual operating expenses of any mutual funds or other investments that the variable annuity holds.

What are some examples of products with combined transaction and ongoing fees?

Some investment products or services, including mutual funds, ETFs and variable annuities, commonly include both transaction and ongoing fees as part of the structure of the product or service. You can use the Financial Industry Regulatory Authority, Inc. (FINRA)’s Fund Analyzer to compare the cost of various types of securities, including mutual funds and ETFs.

What other fees might I pay?

In addition to commissions, a broker-dealer may also charge certain additional fees such as fees for not maintaining a minimum balance, account maintenance, account transfer, account inactivity, wire transfer or other fees. These fees may not always be obvious to you from your account statement or confirmation statement. You should obtain information about all the fees you are charged and why they are charged. Ask your broker-dealer to explain the fees if you do not understand them.

|

SEC Enforcement Actions. The SEC routinely brings enforcement actions involving fees and costs incurred by investors. Here are some examples of cases the SEC has settled:

|

What can I do if I think my fees are too high?

- Follow up. If your fees seem too high, ask questions. Consider following up in writing if you are not satisfied.

- Negotiate. In some cases, fees are negotiable, so you can talk to your investment professional about reducing them.

- Shop around before you invest. Just like shopping around for the best price on any other product or service, you should consider how much you are paying for investing services. However, to the extent you decide to move to a new firm, you should think about any tax consequences and fees for closing or transferring your account, for example, if you have to sell some or all of your current holdings in order to transfer.

Check the background and registration status of anyone recommending or selling an investment by using the SEC’s Investment Adviser Public Disclosure (IAPD) database, which is available on Investor.gov. If you feel the fees charged to you are excessive, report your concern to the SEC, FINRA, or the North American Securities Administrators Association (NASAA).

Additional Information

Investor Bulletin: Brokers' Miscellaneous Fees

Investor Bulletin: Mutual Fund Fees and Expenses

Investor Bulletin: Investment Adviser Sponsored Wrap Fee Programs

Investor Bulletin: How to Select an Investment Professional

Use the SEC’s Investment Adviser Public Disclosure (IAPD) database, which is available on Investor.gov, to check the registration status of anyone recommending or selling an investment.

Visit Investor.gov, the SEC’s website for individual investors.

Receive Investor Alerts and Bulletins from the Office of Investor Education and Advocacy (“OIEA”) by email or RSS feed. Follow OIEA on Twitter @SEC_Investor_Ed. Like OIEA on Facebook at facebook.com/secinvestoreducation.

The Office of Investor Education and Advocacy has provided this information as a service to investors. It is neither a legal interpretation nor a statement of SEC policy. If you have questions concerning the meaning or application of a particular law or rule, please consult with an attorney who specializes in securities law.